Transfer Pricing

In the world of multinational business, Transfer Pricing is the mechanism used to set the price for goods, services, or intellectual property exchanged between different branches or subsidiaries of the same company.

For Ex: Think of it as a “family internal economy.” If a parent company in the US sells a car engine to its assembly plant in Germany, the price they “charge” each other is the transfer price.

Why It Matters

Transfer pricing is a massive deal for both corporations and tax authorities because it dictates where profits are reported—and therefore, where taxes are paid.

- Tax Optimization: Companies might try to set prices so that profits land in countries with lower tax rates.

- Regulatory Compliance: Tax authorities (like the IRS or HMRC) want to ensure they aren’t losing out on tax revenue.

- Internal Performance: It helps a company see which specific divisions are actually profitable on their own merits.

The “Arm’s Length” Principle

This is the golden rule of transfer pricing. To prevent tax evasion, international guidelines (primarily from the OECD) require that internal transactions must be priced as if the two parties were unrelated.

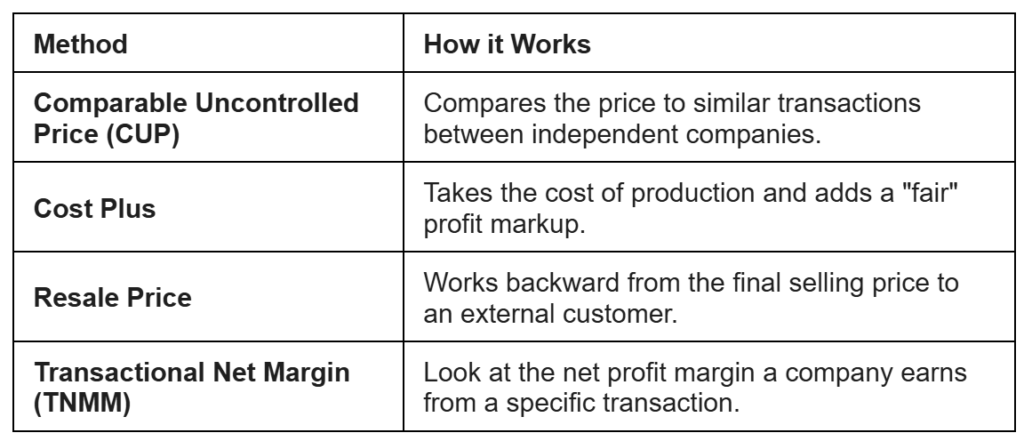

Common Pricing Methods

There isn’t a “one-size-fits-all” approach. Here are the most common ways companies calculate these prices